Why insured crews matter in Massachusetts junk removal

- Joe Lusso

- 1 day ago

- 10 min read

TL;DR:

Insured junk removal crews carry liability, workers’ compensation, and auto insurance protecting property owners.

Massachusetts law and property managers demand proof of insurance to mitigate liability and legal risks.

Verifying insurance coverage through certificates of insurance ensures safe, professional, and compliant services.

Hiring the cheapest junk removal crew you can find seems like a smart move until someone gets hurt on your property, a wall gets gouged hauling out a refrigerator, or a truck drops debris on a neighbor’s car. Massachusetts property owners and managers face real financial exposure every time an uninsured crew steps through the door. One accident, one denied claim, and you could be looking at thousands of dollars in out-of-pocket costs that no one warned you about. This article breaks down exactly what “insured” means in junk removal, why it’s legally and financially critical in Massachusetts, and how to verify coverage before a single item gets moved.

Table of Contents

Key Takeaways

Point | Details |

Insurance is essential | Insured junk removal crews protect property owners from major financial and legal risks. |

Verify before work | Always request a Certificate of Insurance with proper limits and additional insured status before any junk removal begins. |

Better service access | Insured crews can take on bigger jobs, meet commercial requirements, and provide higher professionalism and peace of mind. |

Uninsured means full risk | Hiring uninsured crews puts all liability and potential payment for damages or injuries directly on you. |

What makes a junk removal crew “insured”?

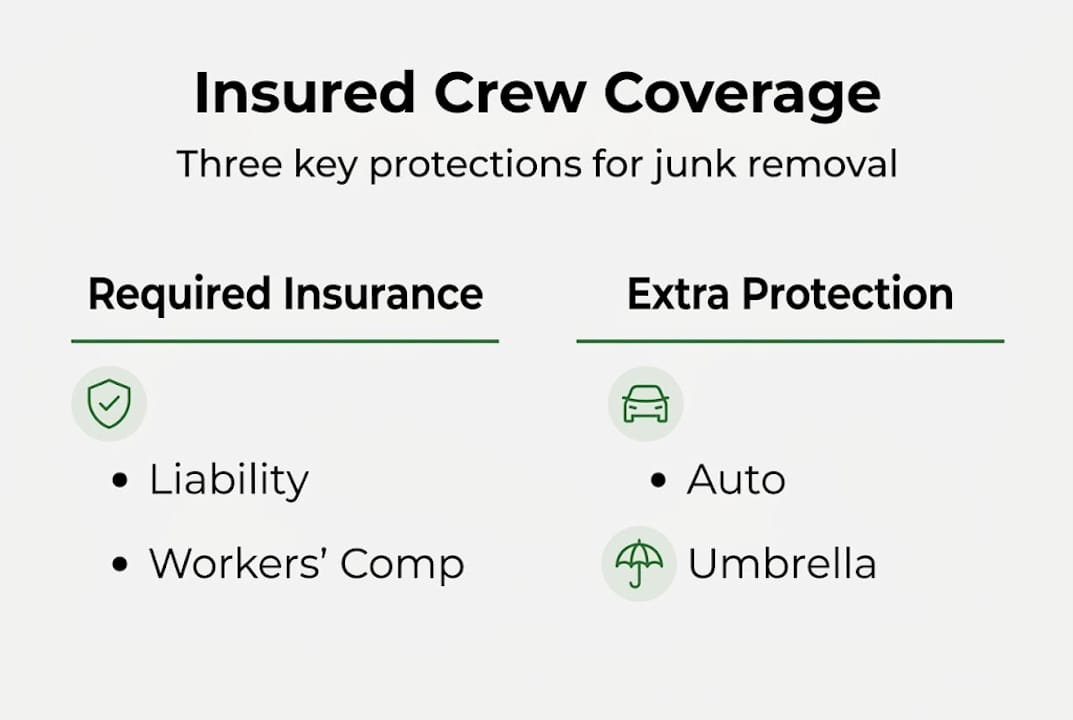

The word “insured” gets thrown around a lot in the home services industry, but it actually refers to a specific set of policies that protect you, the property owner, and the crew doing the work. Not all coverage is created equal, and knowing the difference can save you from a very expensive surprise.

General liability insurance is the foundation. Insured crews carry general liability that covers property damage and bodily injury during operations, including scratching hardwood floors, damaging drywall, or breaking a fixture while hauling heavy furniture. This type of policy pays for repairs and medical costs when accidents happen on your property. Without it, those costs come directly out of your pocket or trigger a dispute that can drag on for months.

Workers’ compensation is equally important. Workers’ comp covers crew injuries from heavy lifting, and commercial auto insurance applies to trucks hauling debris on public roads. In Massachusetts, workers’ compensation is legally required for any business that employs workers, and junk removal crews are no exception. If a worker tears a muscle moving a washer and dryer set from your second floor and the company has no workers’ comp policy, you could find yourself named in a claim.

Commercial auto insurance covers the trucks and vehicles used during the job. Standard personal auto policies do not cover commercial hauling, so a crew driving an uninsured truck is one fender bender away from a significant liability gap.

Here’s a quick breakdown of what each policy type covers:

General liability: Property damage, third-party bodily injury, legal defense costs

Workers’ compensation: On-the-job injuries to crew members, lost wages, medical bills

Commercial auto: Accidents involving hauling vehicles, cargo damage, road liability

Understanding insurance in home services also means recognizing that credible crews will carry all three, not just one.

Pro Tip: Before any crew starts work, ask for a Certificate of Insurance (COI) directly from the company. Don’t just accept a verbal assurance. A real COI lists the policy type, coverage limits, and expiration date. If a crew hesitates or stalls when you ask, that tells you everything you need to know.

Smart property management success starts with knowing which vendors carry the right protection and building that into your vendor approval process from the beginning.

Why insurance is non-negotiable for Massachusetts property owners

Massachusetts has some of the more stringent property liability rules in the country, and commercial property managers feel that pressure most acutely. Understanding what’s required, and what happens when requirements aren’t met, changes how you evaluate every service provider you bring on site.

Commercial property managers in Massachusetts typically require proof of insurance with limits of at least $1 million per occurrence and $2 million in aggregate general liability. They also require that the client be listed as an additional insured on the policy before allowing access for junk removal. That’s not a preference. It’s a contractual requirement for most commercial leases and property management agreements.

“When an uninsured crew causes damage, the property owner often has no legal recourse against the crew. Instead, they absorb the loss, fight a small claims battle, or turn to their own property insurance, which can raise their premiums for years.”

Uninsured crews expose property owners to full liability for accidents, and their uninsured status disqualifies them from commercial bids and contracts, damaging their credibility. For you, hiring them puts your own credibility and finances at risk too.

Think about a practical scenario. A property manager in Worcester hires an uninsured crew to clear out a vacant commercial unit. A crew member falls down a staircase carrying a heavy desk. There is no workers’ comp policy. The worker sues the property owner directly. Legal fees alone can exceed $20,000 before the case is settled, and that’s before any damages are awarded.

Here’s what to check before allowing any crew to begin work:

COI with adequate limits: At minimum $1M per occurrence for commercial jobs

Additional insured endorsement: Your name or company listed directly on the policy

Workers’ comp confirmation: Especially critical if more than one worker is on site

Commercial auto coverage: Confirm trucks are covered for hauling

Policy expiration date: Confirm coverage is active, not lapsed

Our junk disposal guide for Massachusetts property managers goes deeper into vendor requirements and compliance steps. And if you’re a homeowner wondering why this matters for residential jobs too, the homeowner safety and value breakdown covers the residential side in detail.

Skipping this verification step may seem like a time saver. It rarely is. A few minutes reviewing a COI is always worth more than the hours spent managing an uninsured claim.

What insurance protects: Common claims and real-world costs

So what can actually go wrong, and what financial impact does it have? Let’s look at the types of incidents insurance covers and why skipping protection can cost dearly.

General liability runs $500 to $2,000 per year, commercial auto runs $1,500 to $4,000 per vehicle, and workers’ comp costs between $1,000 and $4,000 per employee annually. Those numbers sound significant for a service company, but they’re modest compared to what a single claim can cost without them. A broken glass door, for example, can run $4,500 or more to replace, and that’s a minor incident by industry standards.

Beyond on-property accidents, there’s road risk to consider. Unsecured loads cause roughly 53,000 crashes and 5,500 injuries annually across the United States. A junk removal truck that isn’t properly covered leaves everyone exposed, including bystanders and the property owner who hired the crew.

Here’s a comparison of what insured versus uninsured scenarios actually look like when something goes wrong:

Scenario | With insured crew | With uninsured crew |

Crew scratches hardwood floors | Insurance pays repair costs | You pay out of pocket |

Worker injured on your property | Workers’ comp covers the claim | You may face a lawsuit |

Truck damages a parked car | Commercial auto covers it | Driver or owner pays, or you get dragged in |

Glass door broken during haul | General liability claim filed | $4,500+ cost falls on you |

Property damage dispute | Insurance company handles it | Lengthy legal dispute, no clear remedy |

Pro Tip: Even “small” incidents like breaking a glass panel or nicking a countertop can spiral into thousands of dollars. Don’t assume a crew will pay voluntarily if there’s no insurance policy forcing the issue. Having their insurer in the picture creates a structured, enforceable process.

Reviewing junk removal safety in Massachusetts helps you understand the full spectrum of risks involved. You’ll also want to think about how debris removal connects to facility upkeep and asset protection over the long term.

Insurance and credibility: Why coverage unlocks better service and access

Beyond protection, insurance is a stamp of reliability and a requirement for many commercial opportunities. Property managers, building owners, and contractors routinely screen out uninsured vendors before a conversation even begins. Insurance isn’t just a safety net. It’s a filter for quality.

Commercial property managers require a COI with $1M/$2M general liability and additional insured status as a baseline. Crews that can’t provide this documentation simply don’t get access to the job site. For property managers working with multiple vendors across multiple properties, this is a straightforward rule that saves time and reduces risk exposure.

An uninsured company risks financial ruin from a single claim, while an insured crew brings peace of mind, professionalism, and eligibility for larger commercial contracts. The gap between the two isn’t marginal. It’s the difference between sustainable business operations and one bad day ending everything.

Here’s how the advantages stack up:

Factor | Insured crew | Uninsured crew |

Commercial job eligibility | Yes, widely accepted | Often rejected outright |

Client trust level | High, verifiable | Low, unverifiable |

Project size access | Large and small | Usually small, informal only |

Dispute resolution | Structured insurance process | No formal process |

Repeat business potential | Strong, professional reputation | Risky, unpredictable |

For property managers who want to verify insurance before hiring, here’s a step-by-step process that protects your interests:

Request the COI upfront. Ask for it before scheduling. Any legitimate company will provide it immediately.

Check policy limits. Confirm general liability is at least $1M per occurrence for commercial work.

Verify additional insured status. Your name or entity should be listed, not just referenced.

Contact the insurer directly. Call the number on the COI to confirm the policy is active and not lapsed.

Check workers’ comp separately. Ask for that certificate specifically. It’s often a separate document.

Confirm commercial auto coverage. Especially important for large cleanouts with multiple truck loads.

Exploring local waste management options is useful, but pairing that knowledge with a credible, insured provider is what actually protects you. Our breakdown of commercial junk removal in Massachusetts covers how to evaluate vendors for bigger projects, and understanding safety and compliance standards for junk disposal in the state gives you a stronger foundation for making those calls.

Best practices: How to ensure you hire properly insured crews

Finally, understanding is only half the battle. Here’s how to put your knowledge to work and make confident, compliant hiring decisions every time.

Property owners should request a COI with adequate limits and additional insured status before permitting access. This isn’t just good practice. It protects your revenue, your reputation, and your property from situations that are entirely avoidable with the right upfront steps.

Here’s a step-by-step verification process you can use for every new junk removal vendor:

Call or email before booking. Ask directly: “Do you carry general liability, workers’ comp, and commercial auto insurance?”

Request the COI. A professional company will send it same day. Delays or excuses are red flags.

Review the documents carefully. Check limits, dates, and covered operations.

Ask to be listed as additional insured. This protects you directly, not just the crew.

Store the COI in your vendor file. Keep it accessible in case a claim arises later.

Watch for these red flags when evaluating junk removal crews:

Vague or evasive answers when you ask about insurance types or limits

Expired COI documents or policies listed with lapsed dates

Unusually low limits, such as $100,000 liability on a commercial property job

Reluctance to name you as additional insured

No workers’ comp listed when the crew has multiple employees

No commercial auto coverage despite operating multiple hauling vehicles

Pro Tip: Confirm your additional insured status in writing, ideally as an endorsement on the policy, not just a note on the COI. That endorsement is what gives you direct protection if a claim is filed during the job.

Managing business efficiency in property management means building insurance verification into your standard vendor onboarding checklist. Treat it the same way you treat a contractor’s license or a vendor’s W-9. It’s non-negotiable, not optional.

What most people miss about insured junk removal crews

Here’s the honest truth that most property owners don’t hear enough. The push to save $50 or $100 by hiring the cheapest crew on the market is one of the most expensive decisions a property manager can make. We see it regularly. A client cuts corners on hiring, an accident happens, and suddenly they’re dealing with a dispute that costs ten times the original savings.

An uninsured company faces financial ruin from a single major claim, and property owners who hire them are exposed to the same risk with even less control over the outcome. What’s often missed is that insurance isn’t just about worst-case scenarios. It signals the kind of crew that trains properly, maintains equipment, follows safe hauling practices, and respects your property. Insurance and professionalism travel together.

The Massachusetts market is also shifting. Sustainability standards, liability awareness, and tenant expectations are all pushing property managers toward higher-quality vendors. An eco-friendly junk removal approach matters more now than it did five years ago, and so does the credibility of the crew delivering it. Clients who discover that their property manager used an uninsured vendor don’t forget it. Insurance coverage is increasingly a baseline expectation, and the crews that treat it as optional are falling behind.

Choose reliable, insured junk removal for your Massachusetts property

You’ve covered the theory. Now let’s talk about the practical next step for Massachusetts property owners and managers who want to work with crews that actually protect their interests.

At Junk Dispatch, every job comes backed by insured crews, transparent pricing, and a genuine commitment to eco-conscious disposal across Massachusetts. Whether you need a Reading junk removal service, a full Essex County junk removal cleanout, or a complete attic and garage cleanout, we bring the documentation, the professional crew, and the accountability you need to move forward without liability concerns. Get a free estimate online, book same-day when available, and work with a team that treats your property like it matters.

Frequently asked questions

What proof of insurance should I request from a junk removal crew?

You should always request a Certificate of Insurance showing adequate liability limits and your status as an additional insured before allowing any crew to begin work.

Who is liable if an uninsured crew gets injured on my property?

If the crew is uninsured, property owners face full liability for injuries or damages that occur during the removal, which can include legal fees and medical costs.

Is insurance required for all junk removal jobs in Massachusetts?

Commercial property managers require proof of insurance before granting site access, and workers’ compensation is legally required for crews with employees under Massachusetts law.

How much does insurance cost for junk removal services?

Typical annual insurance costs run $500 to $2,000 for general liability, $1,500 to $4,000 per vehicle for commercial auto, and $1,000 to $4,000 per employee for workers’ compensation coverage.

Recommended

Comments